Your Quick Guide to Funeral Insurance in Canada

What is funeral insurance?

Funeral insurance is a type of life insurance policy that helps your loved ones cover funeral expenses and other end-of-life costs. It’s permanent coverage, which means it stays active as long as you continue to pay your monthly premiums. When the policyholder passes away, the funeral insurance pays out a lump sum to the beneficiaries.

What is funeral insurance used for?

Funeral insurance helps ease the financial burden on your loved ones by covering the costs associated with your final farewell. It acts as a financial safety net, ensuring that end-of-life expenses are taken care of during an emotionally challenging time.

But here’s the catch: Final expense or funeral insurance is incredibly expensive. You’ll pay higher monthly premiums than you would for traditional life insurance policies, and you’ll receive a lower payout upon the policyholder’s death.

Here’s an example of how little value funeral insurance provides:

Let's say your premiums are $50 per month and the payout is $10,000 (typical funeral insurance coverage). If you live for 16 years, you'll pay more for your policy than you’d receive from the payout.

$50 per month = $600 per year

$10,000/$600 = 16.7 years

Is funeral insurance worth it?

In short, no. Funeral insurance should only be a final resort. While it doesn’t require a medical exam, it has costly premiums and lower-than-average payout amounts. Putting money aside in a savings account is almost always the better option than spending money on funeral insurance premiums.

However, funeral or burial insurance may be a viable choice if you:

- Have been denied traditional coverage for term or whole life insurance

- Have existing health issues, such as cancer, heart disease, or chronic illness

- Expect to pass away within a short time frame

If none of these scenarios apply to you, we recommend:

- Putting money aside in a savings account for final expenses

- Getting term life insurance. If you're approved, you’ll likely pay lower premiums and leave your beneficiaries with a larger lump-sum payout

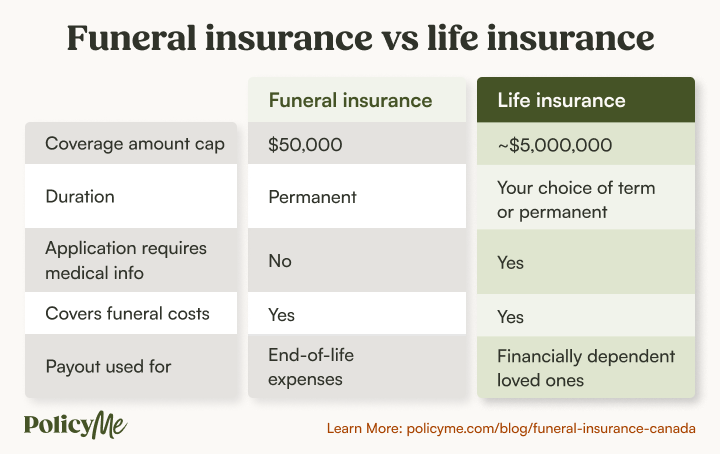

Funeral insurance vs. life insurance

Let's look at a rundown of the differences between funeral insurance and life insurance:

Funeral insurance:

- Covers specific end-of-life expenses, like funeral costs and other final arrangements

- Takes care of things like caskets, services, and burial/cremation costs

- Relieves your loved ones from the financial burden of your farewell

Life insurance:

- Provides broader financial protection for your loved ones

- Offers a payout that can be used for anything your family needs, including paying off a mortgage or covering childcare expenses

- Makes the most sense for those with dependents and significant financial responsibilities

The bottom line: Funeral insurance is designed to cover end-of-life expenses, while life insurance offers broader financial protection for your loved ones.

Read more: How to find affordable life insurance

Can life insurance cover your funeral expenses?

Yes, life insurance can cover your funeral expenses—and anything else your family needs if you pass away. The death benefit for traditional life insurance is much higher than the payout for funeral insurance, so it can provide more comprehensive financial support—covering not just funeral costs, but also debts, living expenses, and future needs for your loved ones.

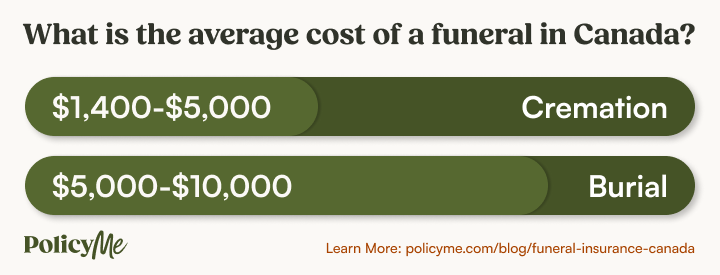

Most life insurance companies offer policies with a death benefit of up to $5 million, though some companies offer even more. The average cost of a funeral is around $8,000, according to data from the National Funeral Directors Association. This leaves your loved ones with a substantial tax-free lump sum to do with as they wish.

Common uses for a life insurance death benefit include:

- Paying off the mortgage

- Setting up a tuition fund

- Taking time off work

- Saving for retirement

Read more: How life insurance works

What does funeral insurance cover?

Funeral insurance has specific uses. The main goal is to help your family cover end-of-life costs, including:

Pros and cons of funeral insurance

Funeral insurance benefits

- Easy qualification: Most funeral insurance plans don't require a medical exam, and some don’t even ask you to complete a medical questionnaire. The application is simple, which is useful for elderly people and those with severe illnesses.

- Fixed premiums: Monthly premiums for final expense coverage remain the same for the duration of the policy, which helps with budgeting.

- Permanent coverage: As long as premiums are paid, the insurance policy doesn't expire.

Funeral insurance drawbacks

- Low coverage amounts: Funeral insurance payouts are typically less than $25,000, which is far less than the average life insurance death benefit.

- High premiums: Monthly premiums for final expense insurance are extremely high, and the total cost of premiums often outweighs the total payout.

Coverage could be redundant: If you already have a term or permanent life insurance policy, there’s a good chance you don’t need final expense insurance.

Types of funeral insurance in Canada

In Canada, there are two types of funeral insurance. Each offers different features, benefits, and eligibility requirements—here’s a quick look at both.

How much does funeral insurance cost in Canada?

Funeral insurance costs vary based on individual factors and the insurance provider. Broadly speaking, though, it can cost about three times as much as a monthly term life insurance premium for a death benefit that’s four times less.

What is the typical funeral insurance payout amount?

The typical funeral insurance payout amount ranges from $5,000 to $50,000—but that maximum death benefit is rarely offered. You'll generally see funeral insurance policies capped at $25,000.

Does the Canadian government help with funeral costs?

The government provides some financial help toward funeral service costs, though the amount of support varies. Here are a few options to explore:

Canada Pension Plan (CPP)

How much you can get: Up to $2,500

Eligibility: You must have contributed to CPP for at least "one-third of the calendar years in their contributory period for the base CPP, but no less than 3 calendar years, or 10 calendar years," according to the Government of Canada. Provincial support may also be available.

Veterans' benefits

How much you can get: Up to $7,376 + tax towards funeral home services

Eligibility: You must have previously served in the Canadian Armed Forces. This benefit is offered through the Last Post Fund, which may also cover the cost of a plot, cemetery charges and burial costs, the cost of cremation, and other related costs. Support is available for headstones for veterans in unmarked graves, too.

Indigenous services

How much you can get: Amounts vary

Eligibility: You must be Indigenous. The government offers estate services for First Nations, and Indigenous communities often have their own programs to help with funeral costs.

Best life insurance companies for funeral insurance

Here's a look at the top three funeral insurance companies in Canada. These are all providers of guaranteed acceptance life insurance policies, which are a type of funeral insurance.

Read our comprehensive review: The best no medical life insurance companies in Canada

FAQ: Final expense insurance for funeral coverage

Jessica is a content marketing manager with PolicyMe. She has over a decade of experience creating content, including 10 years freelancing for nonprofits and small businesses in North America and beyond. She was previously the senior editor handling car insurance content for Silicon Valley startup, and the managing editor for creditcardGenius. She's passionate about breaking down complex financial topics into clear, approachable content that helps readers feel confident about their decisions.

Jessica is a content marketing manager with PolicyMe. She has over a decade of experience creating content, including 10 years freelancing for nonprofits and small businesses in North America and beyond. She was previously the senior editor handling car insurance content for Silicon Valley startup, and the managing editor for creditcardGenius. She's passionate about breaking down complex financial topics into clear, approachable content that helps readers feel confident about their decisions.