Term vs Permanent Life Insurance: What's Right for You?

What’s the difference between term life insurance vs. permanent life insurance?

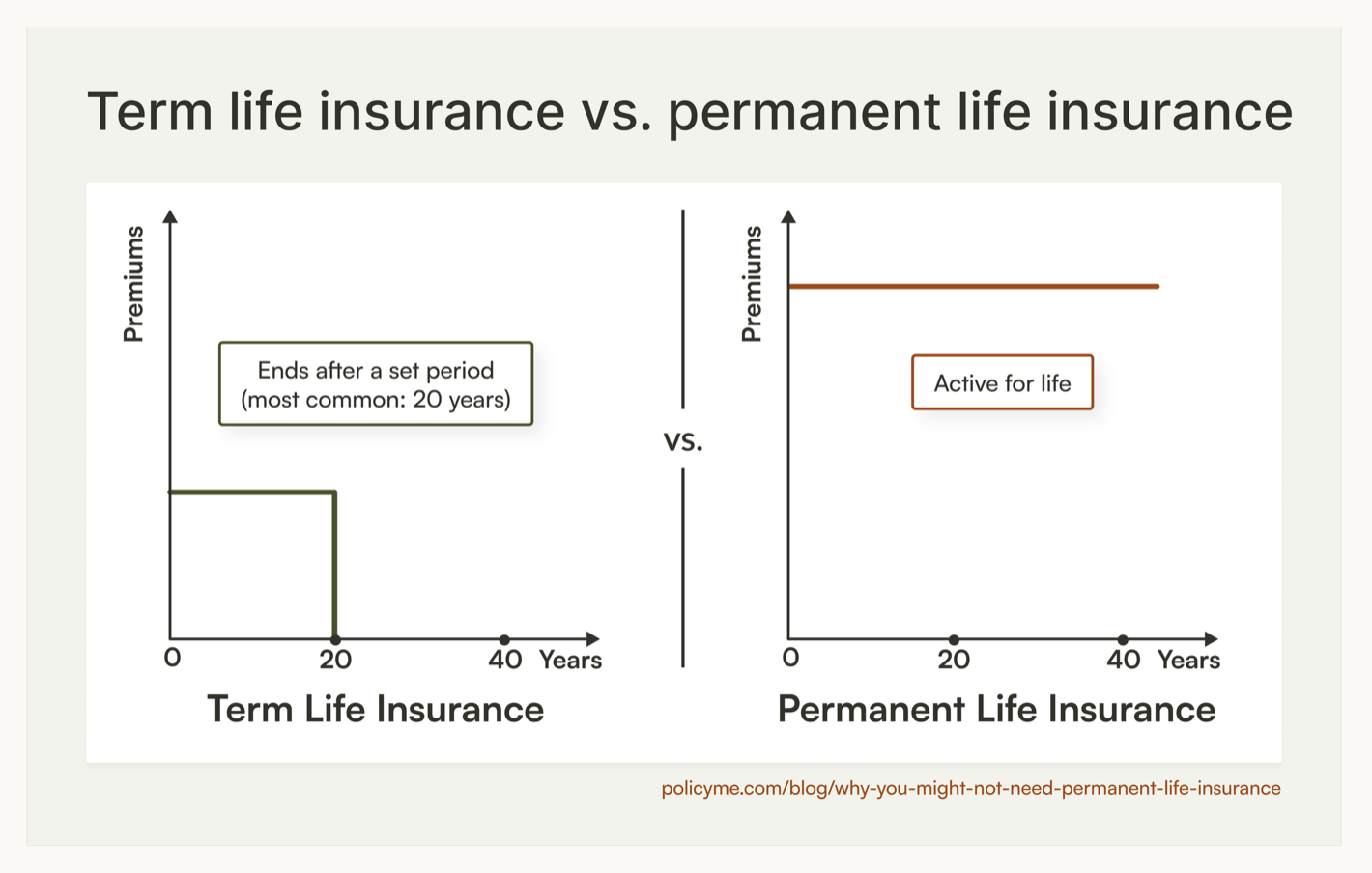

Term and permanent life insurance are the two main types of life insurance policies available in Canada.

The key difference between these two types of policies:

- Term life insurance pays out a tax-free death benefit to your beneficiaries if you pass away during the term’s set period.

- Permanent life insurance covers you for the rest of your life after you activate your policy, providing the death benefit to your beneficiaries regardless of when you pass away.

Term policies are definitely becoming very popular in Canada, especially for those seeking financial protection for temporary obligations. Individual (i.e. not group) term life sales grew 40 per cent in Canada in 2021, more than double that of whole life or universal life insurance.

Let's look at each policy type further.

This quick video is a great primer:

Pros and cons of term life insurance vs permanent life insurance

Life insurance is a smart choice if you have financial obligations that could become burdensome to your loved ones if you pass, but the right type of life insurance policy for you will depend on your financial needs, goals, and stage of life.

Term life offers simple, affordable protection for a set number of years, while permanent life offers lifetime coverage and some financial planning advantages, but at a much higher cost.

Pros of term life insurance

- More affordable than permanent life insurance: Term life insurance quotes are typically much lower, making it accessible for families, homeowners, and young professionals.

- Matches your temporary needs: Ideal for covering expenses that won’t last forever, like raising children, paying off a mortgage, or replacing income until retirement.

- Simple to understand: With no cash value or investment component, term policies are straightforward and easy to manage compared to whole life, universal, or term-to-100 policies.

- Flexibility to convert or review: Some policies offer the option to convert to a permanent policy or renew at the end of the term.

Cons of term life insurance

- Coverage ends after the term: You'll need to renew or apply for a new policy if you still need insurance when your term ends, and this may lead to a higher cost due to age or health changes. But term policies are designed to cover temporary financial obligations, like a mortgage or financial support for young kids, so these obligations will ideally end before your term is complete.

- No cash value: There is no investment component for term life policies, so you won’t receive any return for this policy type.

Pros of permanent life insurance

- Lifelong coverage: As long as you pay your premiums, your beneficiaries are guaranteed a payout, no matter when you pass away.

- Helps with estate planning: Having a permanent life insurance policy could come in handy if you anticipate paying estate tax on your estate when you pass away. Unlike a mortgage, estate tax isn't an expense that you can pay off earlier in life when a term life insurance policy still covers you.

- May support passing on property: A permanent policy could be purchased as a way to offset the eventual life insurance tax liability if you own a second residence and want to pass it on to the next generation.

- Can cover lifelong financial responsibilities: A permanent policy may be something to consider if you know you’ll have lifelong costs, such as a child or other dependent with a disability you support, which may cause your coverage needs to stay level.

Cons of permanent life insurance

- Significantly more expensive: Premiums can be five to 15 times higher than term policies for the same coverage amount.

- Over-insures many Canadians: It assumes you have the same financial obligations forever. If you don't expect to have dependents like young kids, aging parents or debt (e.g. your mortgage) well into the future, why pay life insurance premiums for the rest of your life?

- Lower investment returns: The cash value component typically grows slowly and may offer lower returns than other traditional investment vehicles like TFSAs or RRSPs.

- Complex to manage and understand: With multiple types (whole life, universal life, term-to-100), and varying features, these policies require more effort to maintain and optimize.

- Ties up funds you could invest elsewhere: Paying higher premiums means less flexibility to build wealth through more effective avenues.

Cost comparison: term vs perm life insurance

While life insurance costs vary from person to person, there is an overarching difference between term and permanent life insurance premiums. Permanent life insurance policies are typically up to 10 times more expensive than term coverage because the coverage is guaranteed to pay out and may include a savings or investment component.

Monthly premiums vary based on age, gender, smoking status, health, lifestyle, coverage amount, and policy type.

To put things in perspective, a non-smoking woman aged 30 with $500K in coverage for a 20-term policy can expect to pay around $20.68 per month. And because permanent life insurance can be anywhere from 5 to 10 times more pricey than term, you’re looking at monthly premiums between $103.40 and $206.80.

Is permanent life insurance a good investment?

Permanent life insurance offers an investment component, but this doesn’t mean it’s a good investment. It can seem like a positive feature and a good selling point, but for most people, keeping investment funds in permanent policies doesn’t offer the same flexibility and potential returns that a separate investment fund would.

On top of this, the premiums on a permanent policy are significantly higher than term policy premiums, meaning you’ll have less to invest overall. If you calculate what you’ll pay for a term life insurance policy compared to a permanent one, you’ll find the difference significant.

Next, calculate what you could earn if you invested the cost difference separately, earning interest in a traditional investment account over the next 10 or 20 years.

In most cases, a term life policy is ideal to meet your family’s coverage needs, and you can invest the difference in a separate investment account. This way you have the freedom to control how it’s invested and earn greater returns.

How do I know which type of life insurance is best for me?

The best life insurance policy will depend on your specific financial responsibilities and long-term goals.

If your needs are temporary, like covering your mortgage, replacing income while your kids are still dependent, or providing financial support for a partner until retirement, term life insurance is likely the better fit. It offers affordable coverage and is designed to match the timelines of these common life stages.

For those with lifelong needs, like supporting a dependent with a disability or managing a large estate, permanent life insurance may be worth considering. Just keep in mind that the higher cost only makes sense when those needs are truly long-term.

Who is term life insurance good for?

Term life insurance is a practical, cost-effective way to protect your family during the years they need it most.

Here are some common examples:

- Parents with young children: To replace your income and cover living expenses until your kids are financially independent.

- Couples who rely on each other’s income: To help cover shared expenses while you're still working toward retirement.

- Mortgage holders: To ensure your family can pay off the home if something happens to you before the mortgage is fully paid.

- Business owners: To cover business debts or financial obligations if you're no longer around to manage them.

- Couples nearing retirement without sufficient savings: As a safeguard while building your retirement cushion.

- Those supporting elderly parents: To protect your loved ones from financial strain if you're the primary caregiver or income provider.

Who is permanent life insurance good for?

If you have permanent life insurance needs, like a disabled child or are an exceptionally high income earner, a whole life policy might make sense. Here are a few scenarios:

- High net worth individuals ($10M+ in assets): There are tax-deferred benefits for those that have already maxed out TFSA and RRSP accounts

- Canadians with complex estate planning needs: To protect the value of the estate to maximize the inheritance you pass on

- People who need a forced way to save for retirement: But this should not be a standalone retirement saving strategy

FAQ: Term vs. Permanent life insurance

Jaya is a researcher and writer with 3 years of experience in insurance and finance. She writes in-depth content that bridges technical expertise with accessible insights. Her work spans topics such as life insurance, health and dental coverage, car insurance, and financial literacy, helping Canadians make informed decisions about their financial protection. With a background in market research and editorial strategy, she collaborates closely with subject matter experts to ensure accuracy, clarity, and value in every piece.

Jaya is a researcher and writer with 3 years of experience in insurance and finance. She writes in-depth content that bridges technical expertise with accessible insights. Her work spans topics such as life insurance, health and dental coverage, car insurance, and financial literacy, helping Canadians make informed decisions about their financial protection. With a background in market research and editorial strategy, she collaborates closely with subject matter experts to ensure accuracy, clarity, and value in every piece.